CSRD-compliant reporting

How companies can best set up the process of preparing reports

Comply with current legislation

The Corporate Sustainability Reporting Directive (CSRD) supports the measures of the European Green Deal and is part of the Sustainable Finance set of measures. The expansion of the previous guidelines in Germany now affects companies with a balance sheet total of 25 million euros, net sales of 50 million euros and at least 250 employees. By January 1, 2026, small and medium-sized capital market-oriented companies must submit their first complete, audited report for the 2025 reporting year.

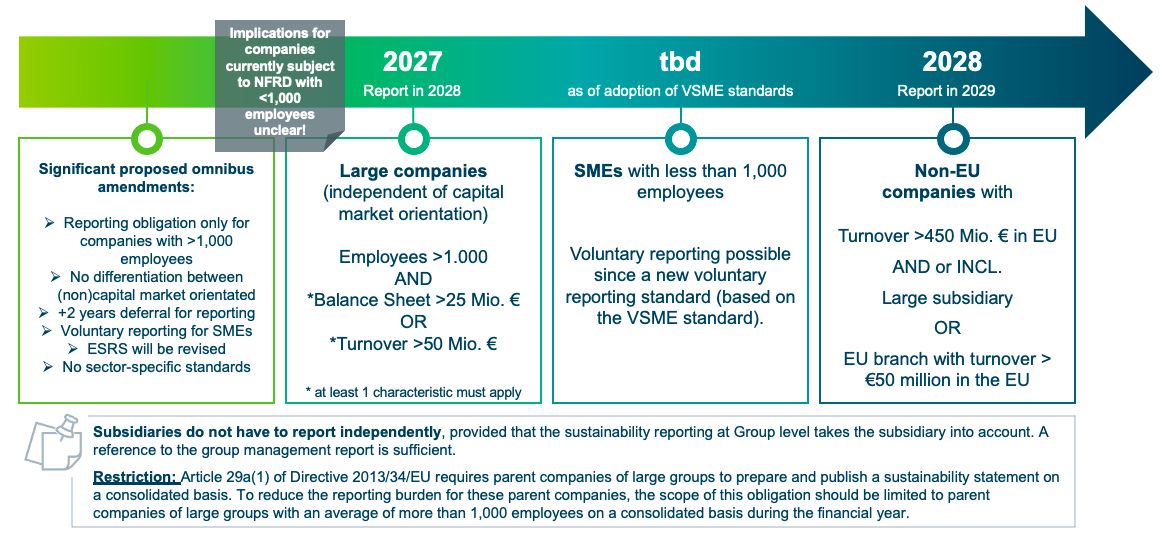

The following dates apply to all other companies:

Why investing in a good report is worth it now

It is right to deal with everything that is necessary now and to distribute responsibilities. Many departments, management, service providers and auditors are involved in the preparation of a comprehensive report. It is worth investing in the process, as companies face it every year.

If employees know what the report is good for internally and externally and how much more than a tedious duty it can be, the likelihood of a good result increases enormously. While companies meet their disclosure obligations with a CSRD-compliant report, companies with a good report can:

- Help shape EU climate goals

- Identify company-specific development potential through data

- Present sustainable developments in the company strategy and be future-proof

- Underpin employer branding with sustainability

- Develop and expand sustainability communication

- Support competitiveness

A dress rehearsal makes your CSRD report better

Preparing a report requires a lot of resources: responsibilities must be clarified, external partners must usually be identified, processes must be integrated, data must be collected, implementation forms and wishes must be coordinated. Companies that are dealing with non-financial key figures for the first time should start as early as possible. Ideally, a first report is implemented as a pilot project one year before the obligation. By doing so, companies are able to establish processes, are not overloaded with the legally required scope of the report and can ensure that their report is also auditable.

Contact us for a nonbinding initial consultation.

Lisa Wießinger

Director

Phone: +49 151 540 352 62

E-mail: lisa.wiessinger@fors.com